What is the significance of the stall in output and employment early in the fourth quarter of 2011, especially in Quebec?

Posted on February 2012

GDP fell in November…

Real GDP stalled in October and dipped 0.1% in November, after four months of rapid growth which reflected the rebound from supply disruptions in the auto and energy sectors that hampered output in the spring. So the first thing to note is that a pause in growth after the passing of the exaggerated rebound from accidents in itself is not unusual nor worrisome.

The November dip in GDP was a surprise to the consensus forecast of 0.3% growth. A closer look at November GDP reveals a couple of interesting nuances. First, all of the decline originated in the energy sector, which has been the main source of volatility in the monthly numbers throughout 2011. Excluding the direct impact of energy, GDP rose 0.1%. The drop in energy output reflects the combination of unusually warm weather (it was the warmest November on record) and numerous small shutdowns (perhaps firms taking advantage of the drop in demand from the warm weather to do regular maintenance). Since these shutdowns all were brief (unlike the extended shutdown caused by the explosion at the Horizon oilsands plant at the start of the year), output should rebound quickly.

…or did it rise?

It is also interesting for economists --admittedly a breed apart-- that GDP fell 0.1% measured in 2008 dollars but rose 0.1% in 2002 dollars (this can be seen in the difference between the Fisher and Laspeyres indices of GDP that are now available free on Cansim). This is because the energy sector has a relatively large weight measured at 2008 prices when energy prices were at record highs. Revaluing energy output at 2002 prices, when energy prices were low, reduces the weight attached to the output drop in this sector. The reverse occurred for the surge in auto output in November; calculating it at 2008 prices, when this industry was in free-fall, reduces the weight attached to growth in this sector, but revaluing it at 2002 prices increases its importance in GDP.

Put both these factors together—the direct impact of energy lowering GDP by 0.2% and the exaggerated impact of this drop at 2008 prices—and the consensus would have been met.

Besides these technical considerations in output, let’s look at how the three major sectors of private demand are performing, namely household, business and export demand.

Household demand rose steadily

Household spending continued to advance steadily in both October and November, with retail sales and existing home sales posting solid gains. Housing starts dipped due to a drop in the volatile multiples component. So not much to worry about in household demand.

While it was widely-publicized that Canadians were more worried about the outlook for 2012 than in any year in the past two decades, other measures of consumer confidence remain at high levels and are consistent with the actual spending of Canadians.

Exports dipped in October before a recovery

A dip in exports was the most obvious source of the monthly weakness in GDP in October. However, there was little to suggest that this drop reflects the recent turmoil emanating from Europe. Exports to the EU did fall in October before leading a rebound in November. Exports to the US strengthened in both months, which is consistent with a wide range of indicators that the underlying trend of our largest trading partner was improving in the fourth quarter. The underlying buoyancy in the export sector was shown in the rebound in exports in November.

More than anything in the report for US GDP in the fourth quarter, the most encouraging developments for better growth in the US were the surge in consumer credit flows in November and reports of a pick up in small business activity, signs that credit flows were increasing to market segments that have faltered in the recovery.

Firms checked spending early in the fall but recently it has improved

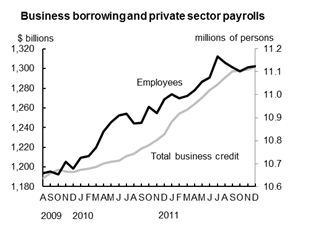

In the view of this newsletter, the most disquieting development early in the fourth quarter was the hesitation of firms to spend and borrow. This was most evident in a dip in private sector payrolls (mostly in Quebec, as will soon be discussed) and a marked slowdown in business fund-raising (both are shown in the first graph below).

Private sector payrolls fell 0.6% between July and October. This would be consistent with firms hesitating to hire in light of the uncertainty surrounding the headlines associated with the delay in raising the US debt ceiling and accompanying downgrade of US debt in August, and the steadily-worsening debt crisis in the EU. However, as it has become clearer that the impact on growth in both Europe and in the US was not as great as initially feared, firms slowly started to hire again in November and December, with private sector payrolls up 0.1%.

Private sector payrolls fell 0.6% between July and October. This would be consistent with firms hesitating to hire in light of the uncertainty surrounding the headlines associated with the delay in raising the US debt ceiling and accompanying downgrade of US debt in August, and the steadily-worsening debt crisis in the EU. However, as it has become clearer that the impact on growth in both Europe and in the US was not as great as initially feared, firms slowly started to hire again in November and December, with private sector payrolls up 0.1%.

Similarly, total business fund-raising slowed to a crawl in October and November, a marked contrast with the rapid gains seen every month since 2009. The good news is that all of this drop appears to be voluntary, unlike the drying up of credit currently underway in Europe which is driven by an unwillingness of banks to lend rather than a drop in demand from firms.

All of the slowdown in October and November originated in a drop in short-term credit, mostly bank loans, and this already began to recover in December. Overall, business credit demand rose $0.6 billion in October, $1.2 billion in November and $2.6 billion in December, a pattern consistent with firms hesitating as global financial markets deteriorated in the autumn but gradually regaining their confidence moving forward.

Most of the job loss was in Quebec

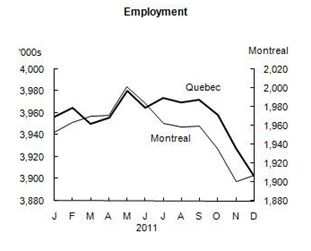

But the real story of the slowdown of employment in the last three months of the year was the dichotomy between job losses in Quebec and 0.4% growth in the rest of Canada in November and December, more than recouping a slight dip in October. Since the weakness was concentrated in Quebec, we will examine it in more detail (note that all the employment data discussed in this newsletter will be slightly be revised on February 3, when StatCan releases its annual revision of seasonal factors used to compute these estimates).

Employment in Quebec fell 1.7% between September and December, worse than any 3-month period even at the worst of the 2008-2009 recession. It was widely noted by analysts that this drop in jobs contradicts all the other major statistics for Quebec on retail sales, manufacturing shipments and exports. Several analysts noted that monthly surveys have a higher amount of noise in them than Statistics Canada likes to discuss in its analysis (the standard error of the monthly employment estimate for Quebec is 15,000; cumulated over three months means that almost all of the 52,000 drop could be sampling error, although it is unlikely this is the entire explanation).

Employment in Quebec fell 1.7% between September and December, worse than any 3-month period even at the worst of the 2008-2009 recession. It was widely noted by analysts that this drop in jobs contradicts all the other major statistics for Quebec on retail sales, manufacturing shipments and exports. Several analysts noted that monthly surveys have a higher amount of noise in them than Statistics Canada likes to discuss in its analysis (the standard error of the monthly employment estimate for Quebec is 15,000; cumulated over three months means that almost all of the 52,000 drop could be sampling error, although it is unlikely this is the entire explanation).

Employment in Quebec could have fallen for plausible reasons

What was not noted by analysts is that Quebec has the largest exposure of its exports to Europe of any major province in Canada (13.3% of Quebec’s exports go to the EU, compared with 10.2% for Ontario and 4.8% in Western Canada). So while exports have not yet felt the impact of a possible slump in EU demand (and that remains conjecture, not a fact), it is conceivable that firms with an exposure to business in Europe decided to batten down the hatches until the fallout from Europe’s crisis became clearer. This is the prudent thing to do; prepare for worst, since it is relatively easy to gear up output if things turn out to be not so bad. This hesitancy would be consistent with slowing business credit demand. However, the Bank of Canada’s survey of 100 large corporations late in 2011 detected no sudden loss of ‘animal spirits’ in executive suites in Canada or Quebec.

There may be other explanations of why Quebec alone lost so many jobs late in the year. Our theory is that it may reflect the chaos on Montreal’s bridges, and there is some evidence this played a role. The data on jobs in Montreal’s CMA show a drop of 52,000 since September, accounting for three-quarters of Quebec’s total loss of 70,000 over that period.[1] More compelling for the ’bridges’ argument is that employment in Montreal peaked in May, and has since fallen steadily for a total loss of 94,000. The drop since May is important, since the closure of whole lanes on the main bridges connecting Montreal to the south shore (and ultimately roads to the US) began in the spring. It is quite plausible that firms in Montreal dependent on truck transport substantially cut back operations this year, or shifted them to other regions. Lesson for governments: good infrastructure matters, so fix the bridges asap.[2]

There may be other explanations of why Quebec alone lost so many jobs late in the year. Our theory is that it may reflect the chaos on Montreal’s bridges, and there is some evidence this played a role. The data on jobs in Montreal’s CMA show a drop of 52,000 since September, accounting for three-quarters of Quebec’s total loss of 70,000 over that period.[1] More compelling for the ’bridges’ argument is that employment in Montreal peaked in May, and has since fallen steadily for a total loss of 94,000. The drop since May is important, since the closure of whole lanes on the main bridges connecting Montreal to the south shore (and ultimately roads to the US) began in the spring. It is quite plausible that firms in Montreal dependent on truck transport substantially cut back operations this year, or shifted them to other regions. Lesson for governments: good infrastructure matters, so fix the bridges asap.[2]

But history suggests the drop was an anomaly

What is most unsettling about the marked deterioration in Quebec’s labour market in the Labour Force Survey is the lack of confirmation from other major economic indicators.[3] Retail sales growth in Quebec in both October and November exceeded the national average over the two months, which would be quite unusual for a population supposedly losing jobs at a rate normally seen only during severe recessions. And manufacturing sales and exports from Quebec showed no sign of the sort of disruption seen in employment in Montreal.

It is instructive to look at past instances where Quebec’s employment fell for extended periods of three or more months; this occurred in 1977, 1983, 1989, 1996, 2003, 2005 and 2006. In every case, the job loss in Quebec was not a harbinger of weakness in the rest of Canada, which continued to grow steadily, but was a temporary aberration that in a majority of cases saw all these losses recouped in only two months after the downturn ended.

Even more compelling, since 1991 when the current survey began, retail sales rose in Quebec (sometimes spectacularly, like a 9% gain in 1996) in three out of the four instances where jobs fell for extended periods. In all four cases, retail sales in Quebec outperformed the national average. So either consumers looked past the temporary loss of jobs and kept spending, or more likely the drop in the survey was noise, and consumers actually were holding on to their jobs, which is why they spent with confidence.

The preponderance of the data so far, especially the ongoing strength of retail sales in Quebec, suggests that it is probably best to treat the fourth-quarter job loss as a bit of a statistical anomaly, consistent with Quebec’s labour market no longer outperforming the rest of the country and possibly reflecting its greater exposure to Europe. But don’t be surprised if there was a bounce-back early in the new year[4].

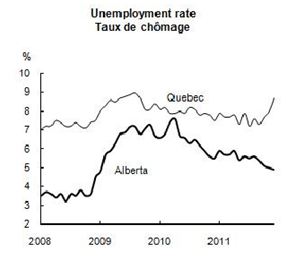

In a reversal of how Quebec fared better during the recession, it is now masking steady growth in jobs in the rest of Canada. The sudden drop in Quebec’s employment was reflected in a surge in its unemployment rate, from 7.1% in September to 8.7% in December. As was widely-noted, Quebec suffered less during the 2008-2009 recession, when its unemployment rate rose by less than two percentage points. By comparison, the boom in Alberta turned into a spectacular crash, with unemployment doubling to 7.5% by April 2010 (versus 7.9% in Quebec), nearly as high as Quebec’s unemployment rate. Since then, the resumption of rapid growth in Alberta’s oilsands has sent its unemployment rate back below 5%, while Quebec has seen its rate return to near its recession high.

In a reversal of how Quebec fared better during the recession, it is now masking steady growth in jobs in the rest of Canada. The sudden drop in Quebec’s employment was reflected in a surge in its unemployment rate, from 7.1% in September to 8.7% in December. As was widely-noted, Quebec suffered less during the 2008-2009 recession, when its unemployment rate rose by less than two percentage points. By comparison, the boom in Alberta turned into a spectacular crash, with unemployment doubling to 7.5% by April 2010 (versus 7.9% in Quebec), nearly as high as Quebec’s unemployment rate. Since then, the resumption of rapid growth in Alberta’s oilsands has sent its unemployment rate back below 5%, while Quebec has seen its rate return to near its recession high.

Summary

The point is not that Quebec’s labour market did not soften late in 2011; the jump in unemployment is significant. Even if employment was flat in the fourth quarter, this still represents a marked slowdown. The real point is that consumers did not behave as if the slowdown was significant, and neither should you. As a footnote, the January data for employment showed a slight rebound in Quebec and a dip in the rest of Canada, the sort of reversion to the mean that one would expect after a large divergence.

The big picture for the overall economy is that the initial pause in business hiring and fund-raising in response to the sea of bad news emanating over the summer from the US and the EU seems to be passing, and business is slowly beginning to resume at a more normal pace.

[1] It is a curious anomaly that employment fell over the last three months in the three largest CMA’s that StatCan publishes on a seasonally adjusted basis; there was a 1.1% drop in Toronto and a 2.8% decline in Vancouver, slightly larger than even Montreal’s drop. There is no obvious explanation for the synchronised drop in all three cities. But with a combined loss of 120,000 jobs, it is a wonder that the national total was down only

0.2% or 36,000 positions.

[2] Another possibility is that some high-tech firms in Quebec have an unusually large dependence on parts from Thailand, which were interrupted by flooding in that country in November. The problem with this theory is that the losses were felt in all industries, not just some segments of manufacturing, and no sudden disruption appears in manufacturing sales in Quebec.

[3] I do not include the small gain in employment in Quebec in October and November in the Survey of Payrolls, Earnings and Hours in the list of indicators that contradict the LFS data. SEPH data do not reflect actual changes in manpower in a specific month, but only when the employees get their first check, which can be months different from when they are hired. The issue of different estimates of employment data in Canada and the US will be addressed in a future newsletter.

[4] I had expected revisions to continue to minimize the seasonal drop in education employment that occurs every summer and the rebound every fall. While the predicted reversion to the mean turned out so far for the employment data in Quebec versus the rest of the economy, this forecast for seasonal factors did not. The good news is that imperfect seasonal adjustment of series make them easy to forecast, so my forecasting record will improve next summer and fall.